This article was authored by Kayla Johnson, Financial Planning Associate.

Planning for retirement involves a lot of considerations – replacing your working income, navigating a sustainable withdrawal rate, planning for healthcare costs and long-term care, estate and legacy planning, as well as tax and gifting strategies (RMD-leveling, withdrawal sequencing, Roth conversions, and qualified charitable distributions) can quickly become complex.

That’s why when it comes to generating an income from your retirement portfolio, simplicity is your friend.

At Pathfinder, the first step we generally recommend is to keep about one year’s worth of spending, that isn’t supplied by income streams like Social Security and pension, in an ultra-conservative investment. This can be advantageous to offset short-term market volatility. This provides a buffer that helps prevent needing to sell during unexpected market volatility if you need quick cash.

Next, we typically recommend using tax-deferred money to fund your regular monthly expenses so you can plan your federal and state tax withholdings correctly. Discretionary and supplemental cash needs can be funded with your non-retirement accounts. You still need to be careful when deciding what and when to sell, as the cost basis and holding period for each position will impact your taxes. Your non-discretionary and discretionary lifestyle expenses will often be funded with a combination of tax-deferred and taxable money, balanced based on careful tax planning.

Once your cash position is in place, and you’ve got a tax-advantageous funding strategy for income, you’ll need to create a plan to periodically refill your cash reserves to maintain adequate funding. This is where careful management of your investment portfolio becomes critical to determine a sequence of withdrawals across your varying account types.

Often, the largest portion of a retirement portfolio comes from tax-deferred retirement accounts, and because 100% of that money is taxable upon withdrawal, you’ll need to monitor your tax situation closely. Unexpected withdrawals from IRAs and 401(k)s can dismantle a great tax strategy, which is why we typically recommend using those accounts for planned expenses. Taxable funds are usually best used next, if the tax planning merits it. Finally, taking tax-free withdrawals from Roth IRAs and Health Savings Accounts (HSAs) for healthcare costs, is usually most advantageous to access last, particularly for unexpected expenses. However, in higher income years, it may be warranted to withdraw from these accounts first and change your regular distribution strategy.

These guidelines are good rules of thumb, but each year of retirement should be managed with the following in mind:

Coastal Land Trust Strikes Deal To Preserve More Than 3,200 Acres Of Sledge Forest

Cierra Noffke

-

Jun 25, 2026

|

|

Refinery Project Eyeing Brunswick County Could Bring $500M Investment, 300 Jobs

Emma Dill

-

Jun 26, 2026

|

|

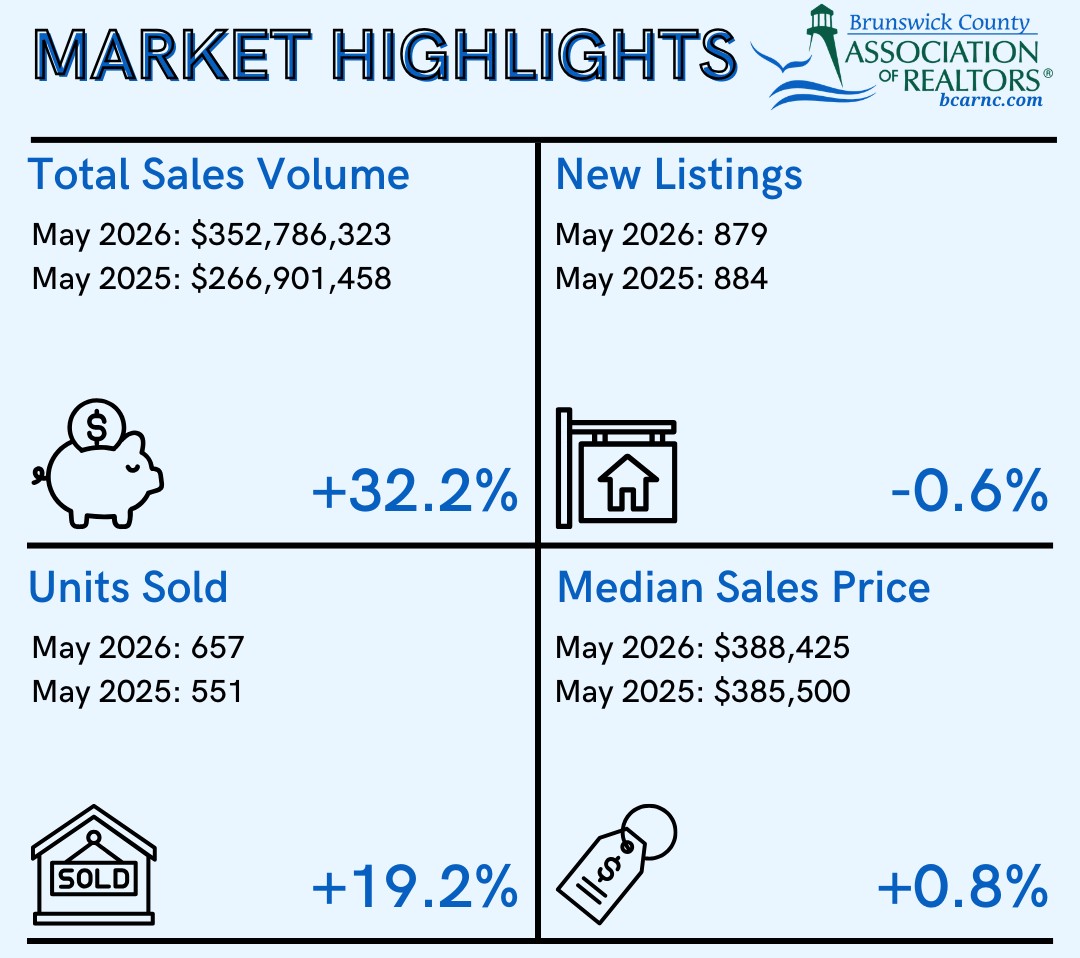

Brunswick Realtors: Home Sales Hit New High In May

Staff Reports

-

Jun 26, 2026

|

|

As Local Firms Exit State Incentive Deals, 2 Remain Active

Emma Dill

-

Jun 25, 2026

|

|

University laboratories are where ideas are born, yet they are often the most overlooked economic engines in North Carolina, writes Jennifer...

The decisions he makes ripple through his organization of over 1,700 employees, into the finance and banking industries, and, in some cases,...

To Darla McGlamery, recent news that an ABC TV series would be coming back to Wilmington to shoot its second season is partly a testament to...

The 2026 WilmingtonBiz: Book on Business is an annual publication showcasing the Wilmington region as a center of business.