This article was contributed by Wealth Advisor John Zachary.

There has been a lot of talk about how the Novant purchase of New Hanover Regional Medical Center (NHRMC) will affect our community. However, what has not been as widely discussed is how the purchase will affect one of the hospital’s greatest assets: its employees. There are several important employee benefit changes that came with the sale, specifically regarding retirement benefits. If you are a current employee of the hospital, this article is for you.

One of the most notable changes with the new benefit structure is the freeze of the defined benefit pension plan. This plan will be replaced by a matching contribution of 6% to the 403(b) retirement savings plan. There are stark differences in these two retirement benefits.

A pension plan promises to provide a formula-based benefit upon retirement, either in the form of a lump sum or a monthly lifetime income payment. Hence why pension plans are also called “defined benefit plans.”

A 403(b) plan, on the other hand, is considered a defined contribution plan. There is no defined benefit at the end, only a defined contribution (the 6% match) on the front end.

The big question is, will the 403(b) 6% match be enough to make up for the loss of the pension plan? As with many answers in finance, it depends. Specifically, in this case it depends on two major factors: your contributions and investment returns.

First, with a pension plan, the employer takes the risk of investing the pension fund money. With a 403(b), the employee holds that risk since they are investing the money on their own. Therefore, the answer to the question posed above largely depends on how your investments grow inside of the 403(b).

In a 403(b) plan, employees have a broad range of investment options. An ultra-conservative investor (someone who leaves their assets in the money market or a cash reserves fund), is unlikely to benefit more from the 6% match compared to the pension, because the assets would be accruing a lower rate of return and likely would not outpace inflation. However, an average investor with a balanced portfolio would have historically earned enough in returns to make the 403(b) match a potentially better alternative to the pension plan. But as noted above, they would also hold the responsibility of maintaining a proper asset allocation and appropriate level of risk.

Another notable difference in the new retirement benefit plan is that, with a typical employer match, the employee must contribute a certain amount into the plan to be eligible for the match. For example, with a pure dollar-for-dollar match, an employee would have to contribute 6% of their own compensation to be able to get the full employer match of 6%. In contrast, with the pension plan, there was no employee contribution requirement. As a financial advisor, I do not see anything wrong with this requirement, since employees should be saving in the 403(b) anyway, but for those who don’t contribute 6%, the pension definitely would have been a better alternative.

In addition to these changes, it has been communicated that employees will have the option of rolling their existing 403(b), 457(b), and/or pension plan lump sum balances into the new 403(b) or an outside IRA (individual retirement account). There are pros and cons for each of those options, and since everyone’s situation is unique, it is critical to evaluate each option before making any decisions.

In summary, since the investment burden is now in the hands of the employees, it is more important than ever for employees to have a solid investment strategy for their retirement funds. In my opinion, the shift from a pension plan to a 403(b) match has the potential to be a suitable alternative to the pension plan, but it is still important to take a comprehensive look at your financial life to know the full impact it will have on your retirement goals.

At Pathfinder, we have worked with hospital employees and leadership for decades. We utilize advanced planning tools to measure how these changes will affect one’s long-term financial plan, as well as to help with pension decisions, such as when to take the benefit and, when it is time, whether to take a lump sum or a monthly annuity benefit. To speak with one of our CERTIFIED FINANCIAL PLANNER™ Professionals about how these changes will affect your long-term plan, give us a call today at (910) 793-0616.

Jason is a wealth advisor and founding partner of Pathfinder Wealth Consulting. He has been in the financial services industry since 1999. Jason was born in Dayton, Ohio, but grew up in Eastern North Carolina. He graduated magna cum laude from the University of North Carolina Wilmington in 1999 with a BS in finance and an MBA in 2003. Rob Penn, Jason’s business partner, hired him in 1999 and the two began a successful business relationship, highlighted by the formation of Pathfinder Wealth Consulting in 2005. Jason’s passion for the business begins with helping our clients, working with select families to accomplish their personal and business goals. Jason’s role also includes managing the overall firm, leading its growth initiatives, and enhancing operations. Jason resides in Wilmington with his wife, Ashley, and their daughter, Merritt. Ashley is a speech-language pathologist and owns Therapy Connections, Inc., a pediatric speech therapy company. Currently, Jason spends most of his free time with his family doing anything kid-related. He also plays average golf as often as possible, waits patiently for his invitation to Jedi training, and hopes that maybe this year he'll have more time for surfing, boating, fishing, and all the water activities that the family loves. Jason considers himself a lifelong learner and is always ready to try a new activity, travel to a new spot, or delve into a new subject.

Coastal Land Trust Strikes Deal To Preserve More Than 3,200 Acres Of Sledge Forest

Cierra Noffke

-

Jun 25, 2026

|

|

Refinery Project Eyeing Brunswick County Could Bring $500M Investment, 300 Jobs

Emma Dill

-

Jun 26, 2026

|

|

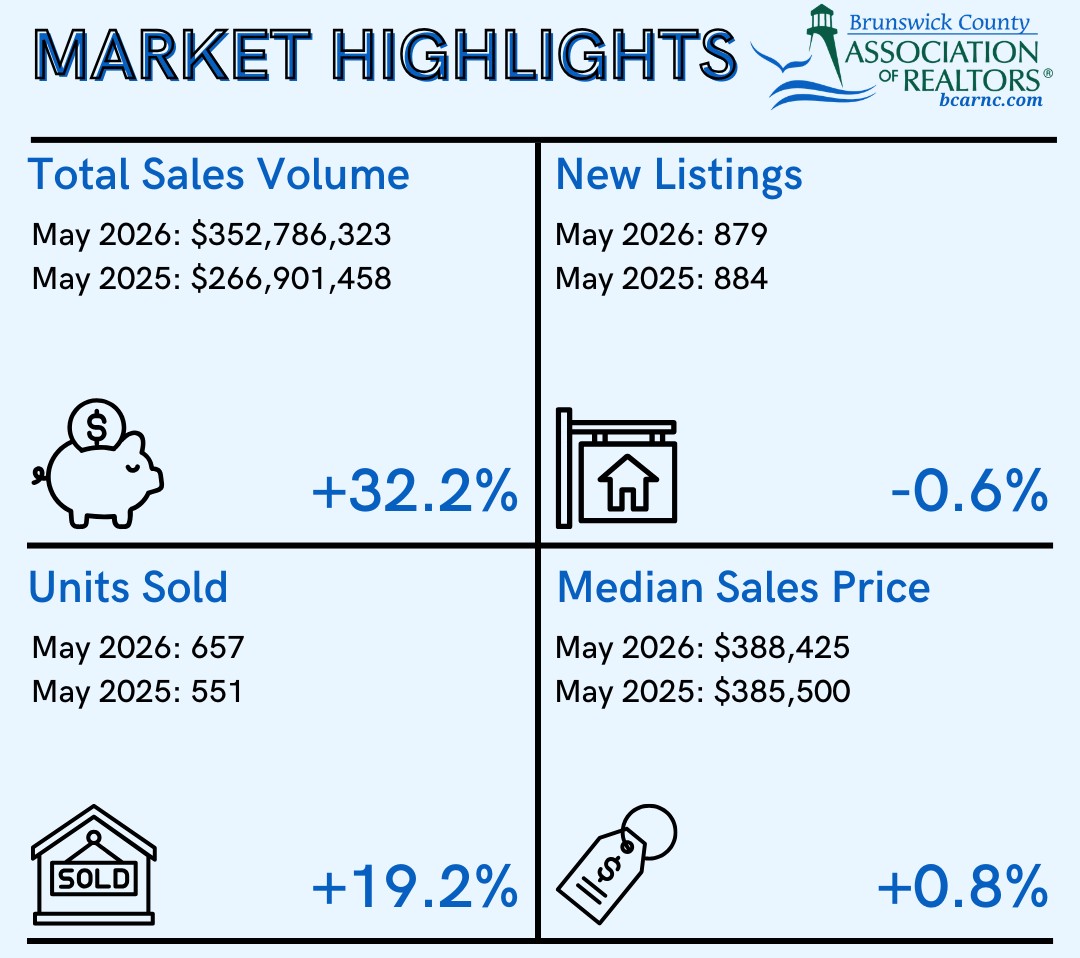

Brunswick Realtors: Home Sales Hit New High In May

Staff Reports

-

Jun 26, 2026

|

|

As Local Firms Exit State Incentive Deals, 2 Remain Active

Emma Dill

-

Jun 25, 2026

|

|

Just as calls from the massive container ships dropped off, port officials began drafting a new strategic plan to guide N.C. Ports....

University laboratories are where ideas are born, yet they are often the most overlooked economic engines in North Carolina, writes Jennifer...

Cybercrime hit home locally when two cyberattacks on the town of Carolina Beach resulted in the theft of nearly $500,000 in December....

The 2026 WilmingtonBiz: Book on Business is an annual publication showcasing the Wilmington region as a center of business.