This Insights article is contributed by Adam McManus, Financial Planning Associate at Pathfinder Wealth Consulting. It is the second in a two-part series on the impact increased life expectancy can have on your retirement. Part I, which defines Longevity Risk, can be found here.

Have you begun saving for retirement? Have you realistically considered your life expectancy?

One of the simplest ways to decrease the risk of longevity negatively impacting your retirement funds is to realistically plan for how long you are going to live and how long your retirement funds need to last. In simple terms, you should plan to live longer than you think, and adjust your retirement savings plan accordingly. If you think you might live until reaching age 90, it is beneficial to plan for living to 93 or 94. This is a conservative approach, but planning to have your retirement funds last longer than they should is a way to protect from outliving your retirement funds.

One of the simplest ways to decrease the risk of longevity negatively impacting your retirement funds is to realistically plan for how long you are going to live and how long your retirement funds need to last. In simple terms, you should plan to live longer than you think, and adjust your retirement savings plan accordingly. If you think you might live until reaching age 90, it is beneficial to plan for living to 93 or 94. This is a conservative approach, but planning to have your retirement funds last longer than they should is a way to protect from outliving your retirement funds.

Hindsight is always 20/20. Why do I say this? A common phrase in our industry is “The best time to start saving for retirement was 20 years ago. The second-best time is today.” One of the simplest strategies to a successful retirement is to begin saving as early as possible. The quicker you begin saving, the quicker you participate in the effect of compounding interest, the "eighth wonder of the world" as Albert Einstein once described.

Obviously, you cannot go back in time and contribute to your retirement accounts, but there are ways to make up those lost contributions. The first is to make sure you are contributing the maximum amount to employer retirement accounts. In 2019, the maximum amount you can contribute to your 401(k), 403(b), and/or 457 is $19,000. The maximum you can contribute to your Individual Retirement Account (IRA) in 2019 is $6,000. Fortunately, there is a Catch-Up Provision that allows people over 50 to make catch-up contributions to their retirement accounts. In 2019, if you are over the age of 50, Catch-Up Contributions Limits allow you to contribute an additional $6,000 to your employer sponsored retirement plan, and an additional $1,000 to your IRA? That is a 31 percent increase of contributions you can make to your employer sponsored retirement plan and a 16 percent increase to your IRA. You may ask yourself, “Should I only take advantage of these catch-up limits if I didn’t start saving as early as I wanted?” The answer is no, every person over 50 can take advantage of these catch-up limits to decrease the risk of longevity in retirement. You can also always save and invest for retirement outside of traditional retirement plans.

Another way you could decrease your risk of longevity is by simply delaying your social security benefits. Persons eligible for social security benefits may file for benefits as early as age 62; however, every year you delay your social security benefits, your benefits increase by 8 percent every year until age 70. If you delay your social security benefits from age 62 to age 70, that is a 64 percent increase in social security benefits for life, in addition to Cost of Living Adjustments that SSA gives each year.

There are also investment strategies to decrease longevity risk as a person moves closer to retirement. A balanced portfolio is a great strategy to mitigate market volatility and consists of roughly 60 percent equity and 40 percent fixed income and limits the floor during a bear market and ceiling during a bull market. A balanced portfolio may reduce long-term growth potential but increases downside protection during markets such as 2007-2009 and the Great Recession. An investor exposed 100 percent to equity may have seen the retirement funds decrease significantly more than an investor only exposed to 50-60 percent equity. Not to mention, if an investor needs money in a time when equities are down, he/she could have fixed income positions to sell from, instead of selling equities when they are down. This can help protect your assets transitioning into distribution phase decreasing longevity risk.

Lastly, there are additional ways to reduce longevity risk utilizing different types of insurance products, such as annuities. These products can be effective and appropriate, but they may be pushed aggressively in the financial industry. We think there are many options that may be effective and wanted to highlight them.

Are you aware of your life expectancy? Do you know how long your retirement funds may last during retirement? Protecting your retirement funds against the risk of longevity is an important factor to consider and is one small part of the comprehensive financial planning process we utilize to help our clients on their financial path to and through retirement. If you are interested in learning more, call us at 910-793-0616 or visit our website for more information.

4018 Oleander Dr, Suite 102, Wilmington, NC 28403 | 910.793.0616 office | 910.793.0617 fax | www.pwcpath.com

Advisory services offered through Commonwealth Financial Network®, a Registered Investment Adviser.

Jason Wheeler is currently the CEO and a Wealth Consultant at Pathfinder Wealth Consulting. Pathfinder specializes in comprehensive financial, estate and tax planning services, investment management, and risk management (insurance) for business owners and successful executives. Jason Wheeler offers securities and advisory services through Commonwealth Financial Network®. Member FINRA, SIPC, a Registered Investment Adviser. To learn more about Pathfinder Wealth Consulting, visit www.pwcpath.com. Jason can be reached at [email protected] or 910-793-0616.

Coastal Land Trust Strikes Deal To Preserve More Than 3,200 Acres Of Sledge Forest

Cierra Noffke

-

Jun 25, 2026

|

|

Refinery Project Eyeing Brunswick County Could Bring $500M Investment, 300 Jobs

Emma Dill

-

Jun 26, 2026

|

|

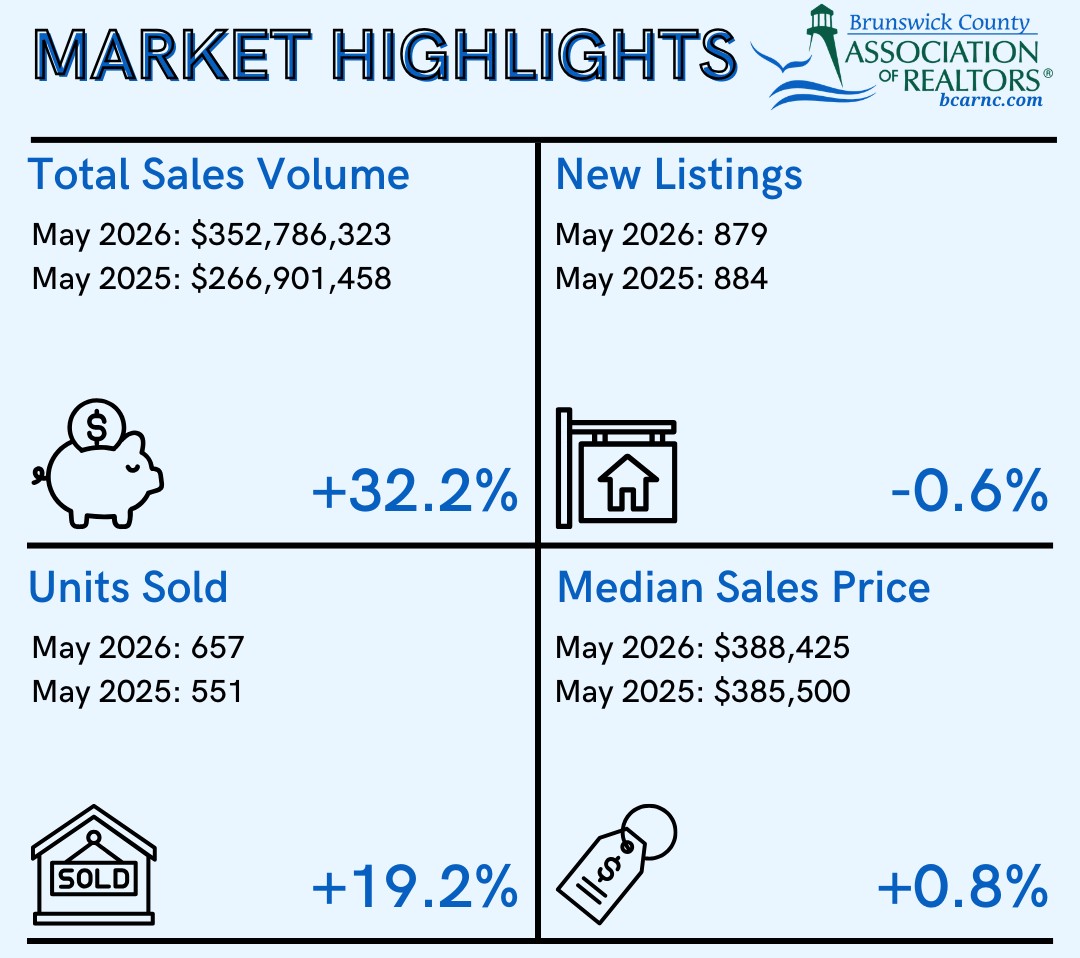

Brunswick Realtors: Home Sales Hit New High In May

Staff Reports

-

Jun 26, 2026

|

|

As Local Firms Exit State Incentive Deals, 2 Remain Active

Emma Dill

-

Jun 25, 2026

|

|

This spring and summer have been a rough time for the city of Southport’s Parks & Recreation Department....

“We’re trying to give control back to the broker,” said the CEO of the Wilmington-headquartered company’s business approach. “We wanted to b...

To Darla McGlamery, recent news that an ABC TV series would be coming back to Wilmington to shoot its second season is partly a testament to...

The 2026 WilmingtonBiz: Book on Business is an annual publication showcasing the Wilmington region as a center of business.