This article is contributed by John Zachary, Wealth Advisor.

If you are still working today, then the answer is, at least in a large part, YOU! Pensions are becoming a historical pastime, so other than social security, income in retirement is largely up to you and your own investments. With the lack of financial literacy already a crisis in our country, that’s a big job to put on individuals.

Some of us have 401(k) plans, or other employer-sponsored retirement plans, that we’ve (hopefully) participated in over the years. But how do you convert that significant amount of savings into a sustainable income stream that will provide for you and your family throughout retirement?

You may have heard about the theory of “safe withdrawal rates” in retirement. Textbooks say that for someone retiring in their mid-60s, a safe withdrawal rate is 4%. This theory is often called the four percent rule.

To give you an idea of how this works, let’s look at an example. Say you’ve worked hard over the past several decades, participated in your company’s retirement plan, and at the end of your career, you have amassed a sum of $2,000,000 in retirement investments. If we use the traditional safe withdrawal rate of 4%, that means you can take $80,000 in income from your portfolio and it should, by theory, withstand the test of time. Inflation protection is built into this theory, with the assumption that the $80,000 could be increased each year to account for inflation. Combine that with any other income sources, such as social security, and there is your gross annual income in retirement.

Seems simple enough, right? Not so much. It’s not only a matter of how much you can draw from a retirement portfolio each year, but also where you get that money from inside of your portfolio.

There’s a lot of information available about tax diversification when you are in the accumulation phase, i.e., putting money into pre-tax savings, Roth (after-tax) savings, and taxable savings buckets. But there’s not as much about how to draw from those savings, specifically, in a sustainable and tax-efficient way.

Sure, you can draw proportionately across your investment portfolio, but in my mind, that negates some of the benefits of a diversified investment strategy. A more prudent method is having a systematic rebalancing approach, constantly looking for opportunities to build up cash for your distributions. At Pathfinder, we recommend that our clients have 6-12 months’ worth of distributions in a safe investment (such as an ultra-short bond fund) not tied to the stock market. I won’t give away all of our secrets, but we also employ an opportunistic rebalancing approach where we take advantage of (upside and downside) market movements to make sure our clients’ income is secure.

In addition, most experts agree that going into retirement, if you plan to draw 4% from your portfolio annually, you shouldn’t have 100% of your investments in stocks. There’s a theory that investing in dividend-paying stocks could provide that 4% without having to sell anything, but that’s at the expense of diversification since that strategy requires that you invest only in dividend-paying stocks.

In a traditional retiree portfolio that contains 60% in stocks and 40% in bonds (often called a 60/40 or a “moderate” portfolio), there will always be a place to draw from. Bonds are relatively more stable than stocks, but they also pay income. Therefore, if we go through a market collapse (where stocks take multiple years to recover), with a 4% withdrawal rate, that’s 10 years’ worth of your distributions sitting in bonds that you can utilize while giving the stocks time to recover. Although all investments come with a certain level of risk, stocks are an important part of most retirees’ investment strategy to grow the portfolio and fight inflation over time.

It is important to note, everyone has a different risk profile. While a 60/40 split is appropriate for most retirement-age investors, it isn’t suitable for everyone. For those who are more conservative, you won’t be able to draw as much from your portfolio, because it simply won’t earn as much as a moderate allocation over time.

The benefit of working with an independent firm that provides fiduciary investment services is that we are held to a higher fiduciary responsibility to work in your best interest. We don’t work for a wall street firm who is there to please shareholders. We work directly for you, the client. Our strategies are tailored to your unique situation, aligned with your goals and your goals only. To learn more about what it’s like to work with an independent fiduciary advisor, and to discuss how to generate a paycheck for yourself in retirement, give us a call at 910-793-0616 or visit our website today.

Jason is a wealth advisor and founding partner of Pathfinder Wealth Consulting. He has been in the financial services industry since 1999. Jason was born in Dayton, Ohio, but grew up in Eastern North Carolina. He graduated magna cum laude from the University of North Carolina Wilmington in 1999 with a BS in finance and an MBA in 2003. Rob Penn, Jason’s business partner, hired him in 1999 and the two began a successful business relationship, highlighted by the formation of Pathfinder Wealth Consulting in 2005. Jason’s passion for the business begins with helping our clients, working with select families to accomplish their personal and business goals. Jason’s role also includes managing the overall firm, leading its growth initiatives, and enhancing operations. Jason resides in Wilmington with his wife, Ashley, and their daughter, Merritt. Ashley is a speech-language pathologist and owns Therapy Connections, Inc., a pediatric speech therapy company. Currently, Jason spends most of his free time with his family doing anything kid-related. He also plays average golf as often as possible, waits patiently for his invitation to Jedi training, and hopes that maybe this year he'll have more time for surfing, boating, fishing, and all the water activities that the family loves. Jason considers himself a lifelong learner and is always ready to try a new activity, travel to a new spot, or delve into a new subject.

Coastal Land Trust Strikes Deal To Preserve More Than 3,200 Acres Of Sledge Forest

Cierra Noffke

-

Jun 25, 2026

|

|

Refinery Project Eyeing Brunswick County Could Bring $500M Investment, 300 Jobs

Emma Dill

-

Jun 26, 2026

|

|

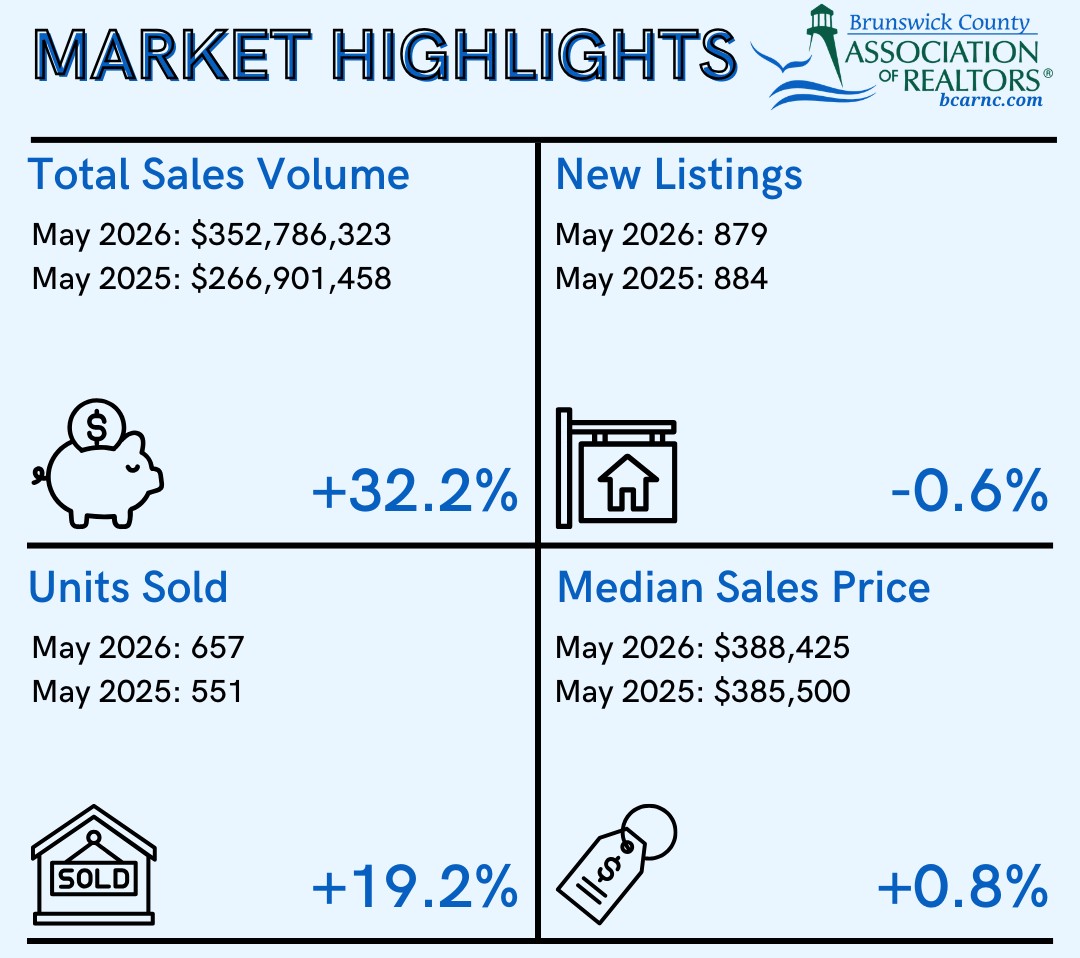

Brunswick Realtors: Home Sales Hit New High In May

Staff Reports

-

Jun 26, 2026

|

|

As Local Firms Exit State Incentive Deals, 2 Remain Active

Emma Dill

-

Jun 25, 2026

|

|

This spring and summer have been a rough time for the city of Southport’s Parks & Recreation Department....

The decisions he makes ripple through his organization of over 1,700 employees, into the finance and banking industries, and, in some cases,...

In February, Chase announced it would be opening more than 160 branches in 30 states this year alone. That includes multiple locations in th...

The 2026 WilmingtonBiz: Book on Business is an annual publication showcasing the Wilmington region as a center of business.