If you could earn and save enough money to meet all of your future financial obligations without taking any risk, would you?

I think it’s important to understand risk taking.

I read an interesting research study recently that listed three major risk domains (along with some subdomains within each major category). They are as follows:

A) Physical status: health and safety risk

B) Lifestyle: social and recreational risk

C) Livelihood: career and finance risk

I appreciate this perspective because it allows me to illustrate some very important behavioral issues when assisting clients with their financial decisions. For example, if someone drinks and smokes regularly, does that mean that they want to free dive 40 miles off the coast? Does investing aggressively mean that you would enjoy a career as a landmine demolition expert? Is it reasonable for an avid skydiver to only feel comfortable investing in certificates of deposit? Is it riskier for an entrepreneur to invest her entire net worth at 27 years of age than it is for an entrepreneur who does the same when he is 67?

The point of these examples is to highlight the fact that there are substantial differences in risk taking across these domains. I think this topic leads to a very important aspect of determining risk in your investment portfolio. I’m not referring to a particular investment risk but rather investor risk.

Historically, risk tolerance questionnaires have been the most widely used tool for determining the amount of equity an investor should have in his or her portfolio. Assessing risk tolerance typically involves having a client answer a set of questions that will determine the optimal amount of investment risk. However, there are many types of assessments and the validity and accuracy of the assessment are heavily dependent on whether or not the right questions are being asked. Which questions are the “right” questions? The right questions are the ones that distinguish between the ability to take on risk and the willingness to take on risk. Once we understand the difference, we can complete a gap analysis to assist clients with trade-off decisions. Here’s how it breaks down:

Ability to take on risk:

Risk capacity: Financial capacity to handle downside results with regards to time horizon, resources and liabilities.

Risk required: Required rate of return to reach your financial goals given the current financial landscape.

Willingness to take on risk:

Risk perception: Subjective judgment about characteristics and scale of risk.

Once we are able to clearly see the differences in the ability and willingness to take on risk, we can perform the gap analysis. The gap analysis overlays a needs analysis with a risk assessment that collectively allows clients to make trade-off decisions. For example, if a client is 18 months from retirement, but she wants to put everything into a speculative investment, trade-off decisions must be made. She may be willing to risk everything, but in reality, she doesn’t have the capacity to take on that much risk.

There are some key issues that surface when assessing risk. The two most prominent are:

Coastal Land Trust Strikes Deal To Preserve More Than 3,200 Acres Of Sledge Forest

Cierra Noffke

-

Jun 25, 2026

|

|

Refinery Project Eyeing Brunswick County Could Bring $500M Investment, 300 Jobs

Emma Dill

-

Jun 26, 2026

|

|

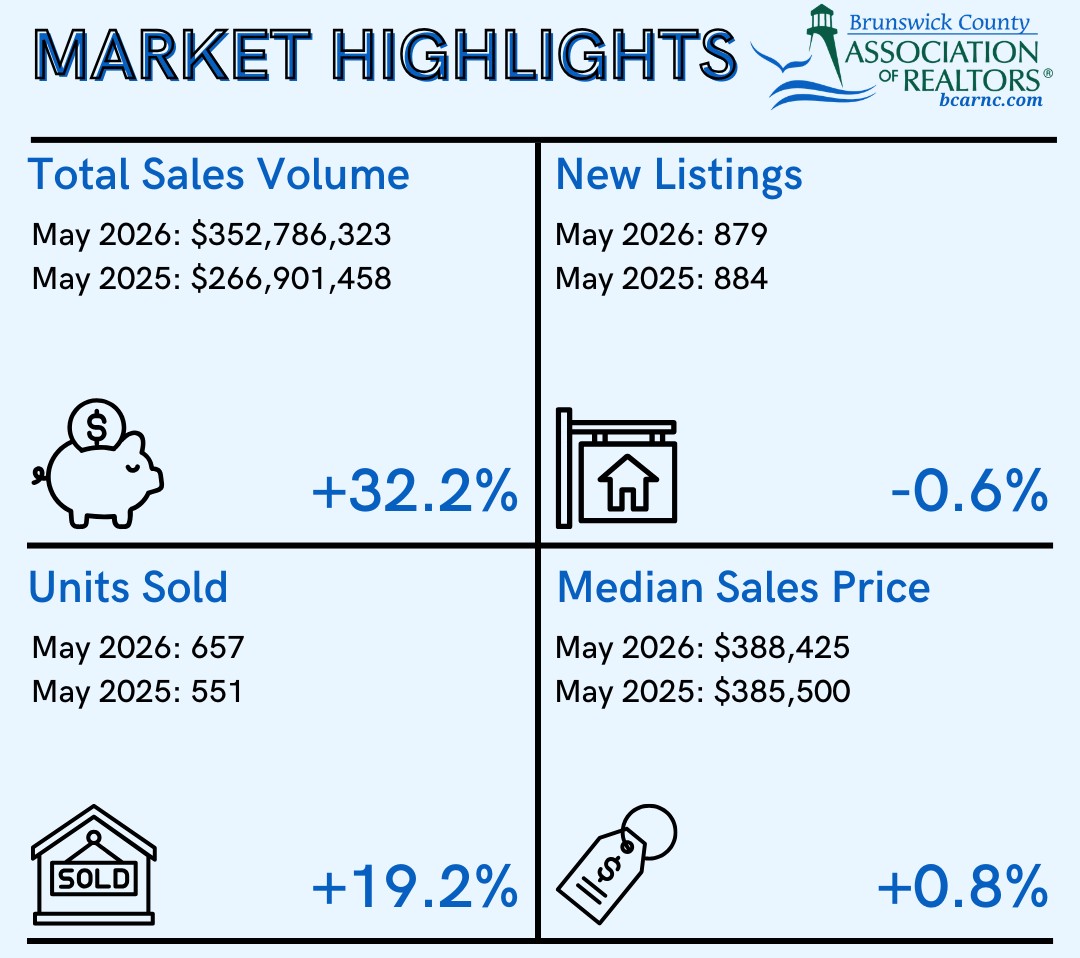

Brunswick Realtors: Home Sales Hit New High In May

Staff Reports

-

Jun 26, 2026

|

|

As Local Firms Exit State Incentive Deals, 2 Remain Active

Emma Dill

-

Jun 25, 2026

|

|

Officials said that the N.C. Fourth of July Festival is an annual fundraising miracle that can’t be taken for granted because there’s no fin...

“More people caring about quality coffee is ultimately a good thing for all of us,” said Kevin Welch, vice president of operations and mark...

“We’re trying to give control back to the broker,” said the CEO of the Wilmington-headquartered company’s business approach. “We wanted to b...

The 2026 WilmingtonBiz: Book on Business is an annual publication showcasing the Wilmington region as a center of business.