This article was authored by Davis Byrd, Financial Planning Associate.

Imagine two people washing their hands. Not a particularly difficult visual in today’s environment, is it? The first person applies soap, rinses their hands, and dries them off. Meanwhile, the second person rinses their hands, applies soap, then dries them off. Yuck. Both people have performed the same tasks in the same amount of time, but only one person has properly washed their hands. Why? Order matters. Similarly, the order in which your investment returns occur can have a dramatic impact on how long a portfolio can sustain a stream of income for a retiree.

While it is true that an investor will receive a particular average return in the long run, it is a mistake to assume that you will earn that same long-term average each year. In other words, you may average 6% over the long run, but you won’t make 6% each year. Returns are expected to fluctuate, and periods of negative returns are not abnormal. In the example below, Bill & Jane both average 6% and both suffered a year when they lost 25%.

But that’s only part of the story. For those who are taking retirement distributions, the sequence in which you receive your annual returns impacts the longevity of your portfolio. To illustrate, consider Bill & Jane, two hypothetical retirees. Both will retire at the same age with portfolios of $1,000,000, withdraw $40,000 at the start of each year, and earn a long-term average of 6% on their investments in their first four years of retirement. The caveat – the order in which their returns occur will be inverse. Note that the annual withdrawals are inflation-adjusted at 2.25%.

| Year | Withdrawal | Bill's Portfolio | Bill's Return | Jane’s Portfolio | Jane's Return |

| 1 | $40,000 | $1,000,000 | 30% | $1,000,000 | -25% |

| 2 | $40,900 | $1,248,000 | 12% | $720,000 | 5% |

| 3 | $41,820 | $1,351,952 | 5% | $713,055 | 12% |

| 4 | $42,761 | $1,375,638 | -25% | $751,783 | 30% |

| $999,658 | 6% | $921,728 | 6% |

Coastal Land Trust Strikes Deal To Preserve More Than 3,200 Acres Of Sledge Forest

Cierra Noffke

-

Jun 25, 2026

|

|

Refinery Project Eyeing Brunswick County Could Bring $500M Investment, 300 Jobs

Emma Dill

-

Jun 26, 2026

|

|

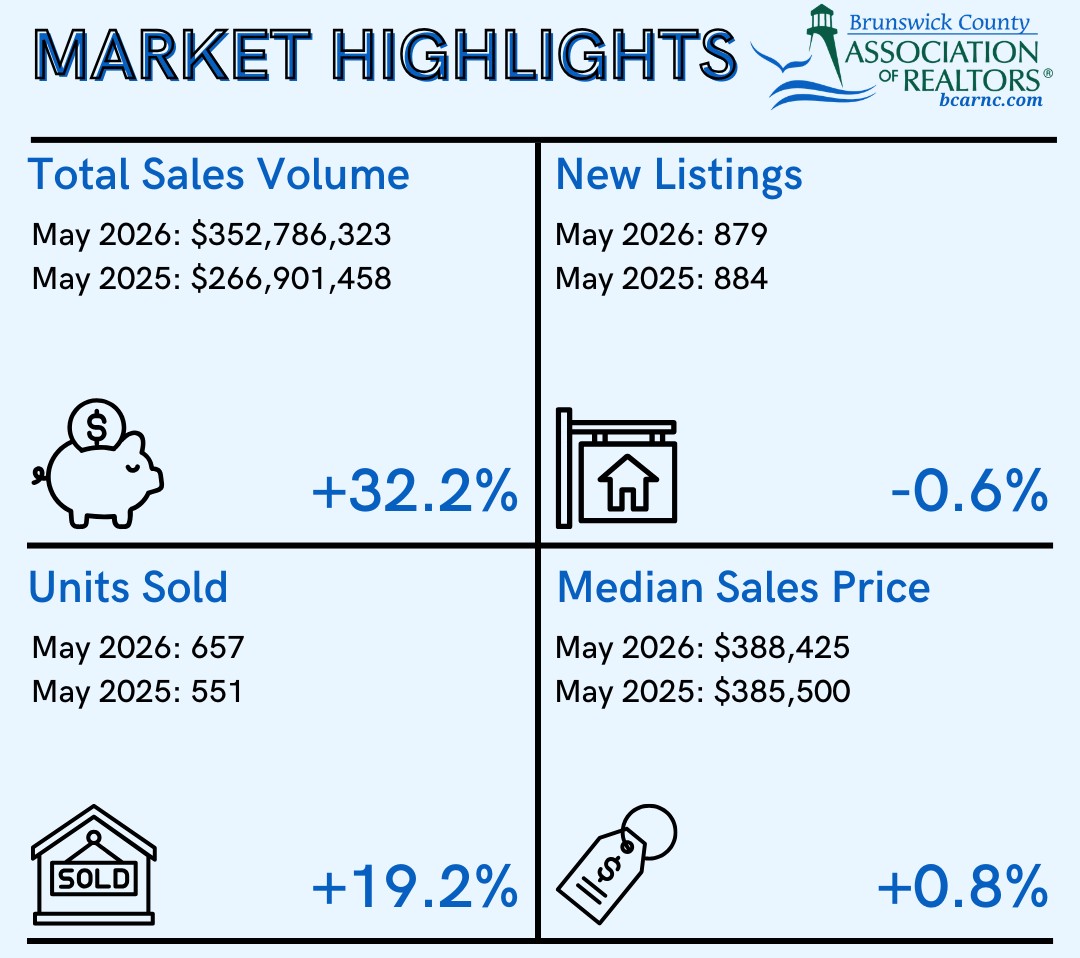

Brunswick Realtors: Home Sales Hit New High In May

Staff Reports

-

Jun 26, 2026

|

|

As Local Firms Exit State Incentive Deals, 2 Remain Active

Emma Dill

-

Jun 25, 2026

|

|

In the past six months alone, a broker with Intracoastal Realty Corp. said he’s sold four lots in the Brooklyn Arts District corridor....

Just as calls from the massive container ships dropped off, port officials began drafting a new strategic plan to guide N.C. Ports....

Creative reuse centers, which function like thrift stores, collect donated materials and resell them to the public at discounted prices to b...

The 2026 WilmingtonBiz: Book on Business is an annual publication showcasing the Wilmington region as a center of business.