This article was contributed by Wealth Advisor John Zachary.

The silent killer. The redheaded stepchild of economists. Inflation has become a big topic in the financial media recently, as it typically does during periods of government stimulus and spending. However, inflation hasn’t been a real risk for a very long time – even decades – so why is it coming into the conversation now?

Before we go into our expectations for inflation in the near term, let’s first cover the basics. Inflation is traditionally measured by something called the Consumer Price index, or CPI. Over the past 20 years, the CPI has averaged around 2.5%. Before the Great Recession of 2007- 2009, CPI averaged around 2-3%. There was a brief spike to around 5% coming out of the crisis, but it has since hovered around 1.5%. In other words, inflation has been largely muted for a very long time. It’s also worth noting that the CPI formula has been adjusted multiple times to account for changes in consumer culture and to increase efficiencies over the years.

There’s another measure of inflation called Core CPI, which is CPI without food and energy. The reason for taking out those two factors is primarily because those two areas tend to have volatile pricing swings. Taking them out gives us a more stable measure of inflation over time. Looking at that measure, inflation has averaged around 2% for the past two decades.

Another measure of inflation, called CPI-E, is an experimental index for those ages 62 and older. It was created to narrow down the expenditures to those of seniors, whose expenses have historically gone up faster than CPI. It has been argued that this should be the measure used to determine social security cost-of-living-adjustments (or COLAs), but that has not yet been implemented since it would put a larger stress on the social security program. Instead, the CPI-W measure is used, which only includes expenditures by those in hourly wage earning or clerical jobs.

Going back to the original point, if the common consensus is that federal stimulus or spending leads to inflation, then shouldn’t there be a correlation between these two metrics? Well, there’s not. If you look back to the early 1990s, over the time that the federal deficit has increased, inflation has decreased. Not to say that an ever-increasing deficit isn’t a problem, but historically it hasn’t caused inflation.

More simply put, inflation isn’t directly correlated to government spending or an easy dollar, it’s dependent upon supply & demand. If supply is rampant but demand is low, prices tend to decrease. Alternatively, if supply is low and demand is high, prices tend to increase (i.e. companies can charge more for goods and services when there are less goods and services available).

And that’s what we’ve seen with the latest inflation increase. The Walt Street Journal reported that U.S consumer prices surged 4.2% in April, the biggest jump in any 12-month period since 2008. Why is that? Consumers are finally getting out and spending money, however, the supply chain has not yet recovered from the pandemic. That means that demand is there, but the supply is not, which has led to an increase in prices. Theoretically, this shouldn’t last long, as factories and manufacturing facilities get back to normal production levels. Once that happens, supply should get back to normal, and therefore, so should prices.

With that said, although we don’t see rampant inflation becoming an issue in the near-term, we do think it’s crucial to factor inflation into your overall financial plan. Even a 2% inflation rate could have a big impact on your spending plans in the future. For example, the average cost of a new car in 2021 is $39,000. With 2% inflation, after 30 years that same vehicle will cost over $70,000!

At Pathfinder, we have been helping our clients navigate the risks of the markets for decades. Whether it’s inflation, recessions, market volatility, or a global pandemic, we have helped to keep clients grounded and financially confident even during the toughest of times. If you’re looking to partner with a firm that can help you look past the financial headlines, give us a call at 910-793-0616.

Jason is a wealth advisor and founding partner of Pathfinder Wealth Consulting. He has been in the financial services industry since 1999. Jason was born in Dayton, Ohio, but grew up in Eastern North Carolina. He graduated magna cum laude from the University of North Carolina Wilmington in 1999 with a BS in finance and an MBA in 2003. Rob Penn, Jason’s business partner, hired him in 1999 and the two began a successful business relationship, highlighted by the formation of Pathfinder Wealth Consulting in 2005. Jason’s passion for the business begins with helping our clients, working with select families to accomplish their personal and business goals. Jason’s role also includes managing the overall firm, leading its growth initiatives, and enhancing operations. Jason resides in Wilmington with his wife, Ashley, and their daughter, Merritt. Ashley is a speech-language pathologist and owns Therapy Connections, Inc., a pediatric speech therapy company. Currently, Jason spends most of his free time with his family doing anything kid-related. He also plays average golf as often as possible, waits patiently for his invitation to Jedi training, and hopes that maybe this year he'll have more time for surfing, boating, fishing, and all the water activities that the family loves. Jason considers himself a lifelong learner and is always ready to try a new activity, travel to a new spot, or delve into a new subject.

Coastal Land Trust Strikes Deal To Preserve More Than 3,200 Acres Of Sledge Forest

Cierra Noffke

-

Jun 25, 2026

|

|

Refinery Project Eyeing Brunswick County Could Bring $500M Investment, 300 Jobs

Emma Dill

-

Jun 26, 2026

|

|

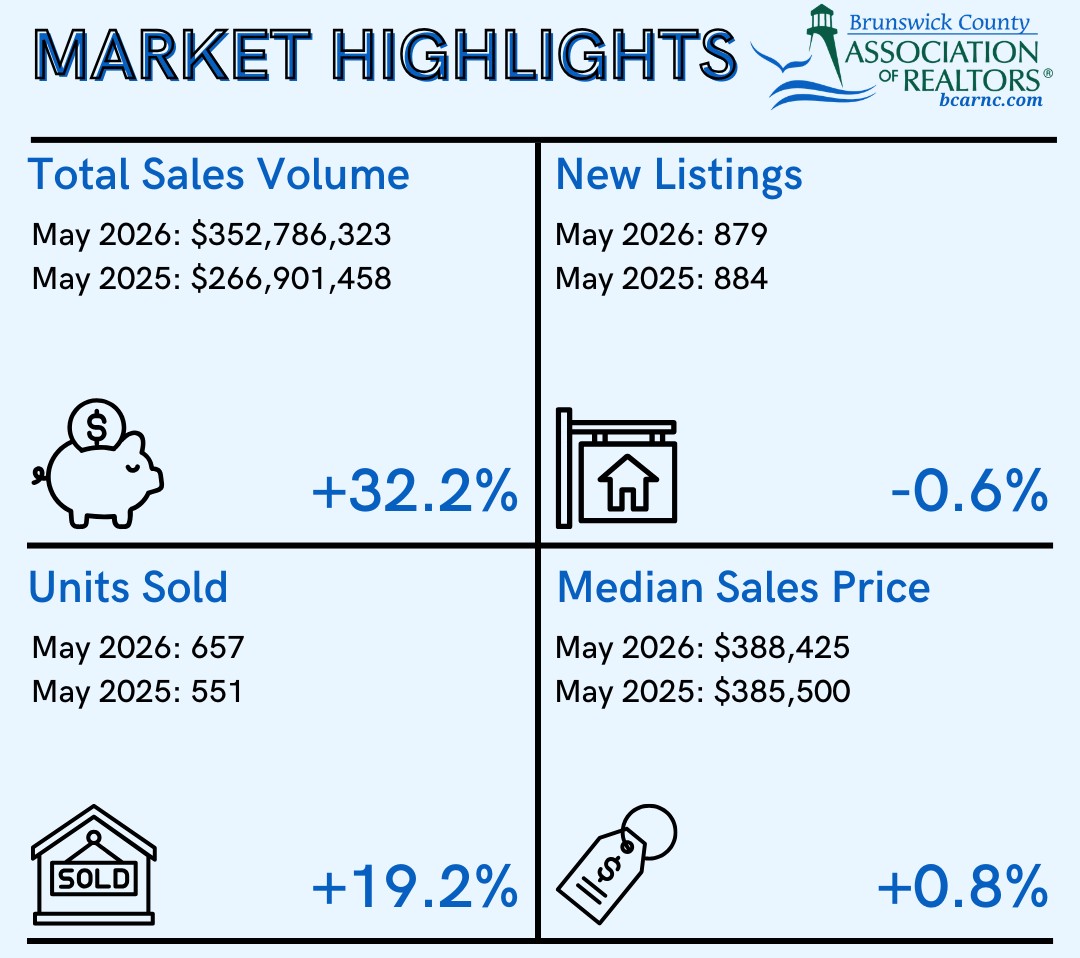

Brunswick Realtors: Home Sales Hit New High In May

Staff Reports

-

Jun 26, 2026

|

|

As Local Firms Exit State Incentive Deals, 2 Remain Active

Emma Dill

-

Jun 25, 2026

|

|

Just as calls from the massive container ships dropped off, port officials began drafting a new strategic plan to guide N.C. Ports....

Officials said that the N.C. Fourth of July Festival is an annual fundraising miracle that can’t be taken for granted because there’s no fin...

This spring and summer have been a rough time for the city of Southport’s Parks & Recreation Department....

The 2026 WilmingtonBiz: Book on Business is an annual publication showcasing the Wilmington region as a center of business.