Over the last month, I have had several people who are planning for retirement come to me with one burning question, “How much will my health care cost?” I have also heard on numerous occasions, and with a weary tone, “Who can retire these days with the cost of health care?” We are all well aware of the effect that rising health care costs are having on our population, and as a result, the Medicare and Medicaid system in general. This is drastically affecting current retirees and, as we commonly refer to them, the baby boomers, who will be (and are already) retiring in droves over the next 10 to 15 years. But, even if you’re not in that category, I would suggest that you keep reading because these points will likely have even more affect on you and your family over your lifetime, and it’s never too early to start planning for them.

According to the Center for Medicare and Medicaid Services, “health spending is projected to grow at an annual rate of 5.8 percent from 2012-2022, 1.0 percentage point faster than expected annual growth in the Gross Domestic Product (GDP)1.” For retirees, many of whom are on a fixed income, this could ultimately mean substantial reductions to their retirement income and purchasing power.

To make the matter worse, when it comes time to enroll in Medicare (most individuals are eligible upon reaching age 65) the complexity of available options is overwhelming. Between Medicare (Part A, Part B and Part D) and Medicare Supplement (which range from Plan A to Plan N), understanding the choices is not easy.

In August, our financial planning software was upgraded with a new Health Care Cost Calculator to help us better plan for health care costs. This powerful new tool allows us to estimate what your medical costs will be using retirement-based information specific to your situation. Accurately estimating retirement and health care costs is a complex undertaking based on many factors. Miss just a few components of the formula and you could find yourself falling short in your retirement savings and income. These factors include any private coverage you have prior to age 65, Medicare part B and D premiums, Medicare supplement premiums (also known as Medigap), and out-of pocket costs, such as co-pays, deductibles and non-covered medical costs.

Medicare Part A covers (up to certain limits): hospital care, skilled nursing care, nursing home care, hospice and home health services. Part A is typically provided at no cost because you (or your spouse) have already paid premiums through payroll deductions while you were working. Part B covers medical insurance, such as doctors’ services and outpatient care. Most individuals pay a monthly premium for Part B. Lastly, Part D covers prescription drug coverage, and also requires a monthly premium. Your premium costs will depend on your MAGI, which is the total of your adjusted gross income (AGI) and tax-exempt interest income (if you’re interested, pull up SSA publication No. 05-10536, which explains this in enough detail to make your eyes water).

To help cover any gaps that exist in coverage, insurance companies offer Medicare supplement or Medigap policies. These policies help cover copayments, coinsurance, deductibles or both. These plans range in benefits and are distinguished by a letter in the alphabet (plans A through N). Learn more here: http://www.medicare.gov/supplement-other-insurance/compare-medigap/compare-medigap.html

The costs for all these coverages are also rising dramatically. According to the 2012 and 2013 Medicare Board of Trustees Report, premiums have increased annually by an average rate of 7.87 percent for Part B; 7.12 percent for Part D; and 5 percent for Medigap insurance.

Out-of-pocket costs may include dental care, vision, hearing and medication costs not covered by the average prescription drug plan. Keep in mind that long-term care expenses are not covered by any of the Medicare or Medigap programs. We have a separate tool that helps us plan for the effects that long-term care expenses can have on your financial plan. There are also long-term care insurance products available, but that is a discussion for another day.

In summary, rising health care costs are likely to have a profound effect not only on retirees, but on our nation as a whole. One way we can better prepare ourselves is to plan for these costs and account for them in our financial plans. One phrase we throw around often is, “People don’t plan to fail, they fail to plan.” We cannot control what the government is going to do, where taxes will be in the future, or where health care costs will be when we retire, but if we sit down and make reasonable assumptions and plan for the unexpected, not only will we be better off as families, but we will be better off as a community and a nation.

If you’re interested in seeing how health care costs might affect when you can retire, feel free to give me a call or shoot me an email.

Jason Wheeler is currently the CEO and a Wealth Consultant at Pathfinder Wealth Consulting. Pathfinder specializes in comprehensive financial, estate and tax planning services, investment management, and risk management (insurance) for business owners and successful executives. Jason Wheeler offers securities and advisory services through Commonwealth Financial Network®. Member FINRA, SIPC, a Registered Investment Adviser. To learn more about Pathfinder Wealth Consulting, visit www.pathfinderwc.com. Jason can be reached at [email protected] , 4018 Oleander Dr. Ste. 2 Wilmington, NC 28403, or 910-793-0616.

Coastal Land Trust Strikes Deal To Preserve More Than 3,200 Acres Of Sledge Forest

Cierra Noffke

-

Jun 25, 2026

|

|

Refinery Project Eyeing Brunswick County Could Bring $500M Investment, 300 Jobs

Emma Dill

-

Jun 26, 2026

|

|

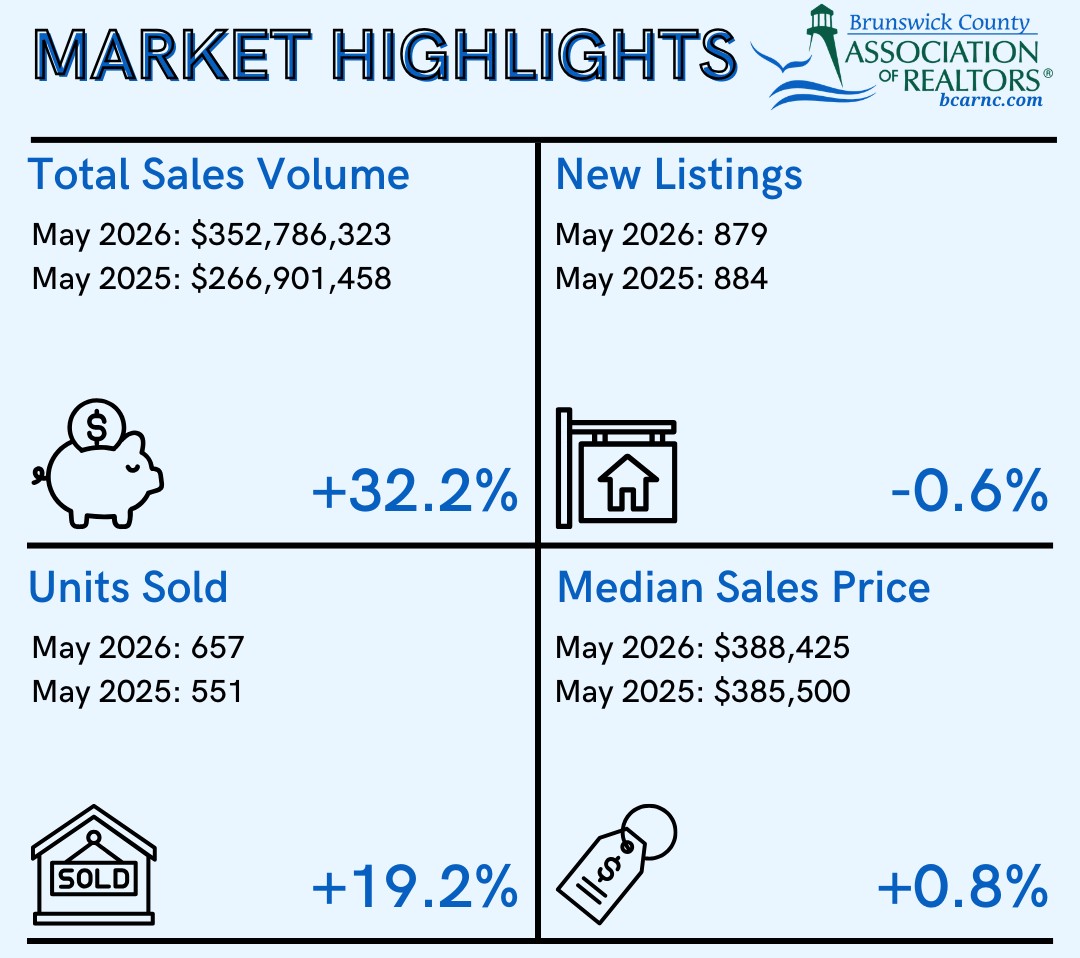

Brunswick Realtors: Home Sales Hit New High In May

Staff Reports

-

Jun 26, 2026

|

|

As Local Firms Exit State Incentive Deals, 2 Remain Active

Emma Dill

-

Jun 25, 2026

|

|

“We’re trying to give control back to the broker,” said the CEO of the Wilmington-headquartered company’s business approach. “We wanted to b...

To Darla McGlamery, recent news that an ABC TV series would be coming back to Wilmington to shoot its second season is partly a testament to...

In the past six months alone, a broker with Intracoastal Realty Corp. said he’s sold four lots in the Brooklyn Arts District corridor....

The 2026 WilmingtonBiz: Book on Business is an annual publication showcasing the Wilmington region as a center of business.