This article is the second of a two-part series examining various ways for business owners to leverage their business profits. If you’d like to read part one, click here.

To recap, in part one we looked at using profits to pay off debts, and we also discussed the importance of spending a little along the way to have a little fun in life.

Part 2 of 2

Now we’re going to review two other popular tactics for getting the most out of business profits: reinvesting it back into the business, and investing it elsewhere.

Profits Option #3 – Reinvesting in your business

Unless lenders are waiting outside the door, knocking incessantly, the first inclination of most business owners is to reinvest profits back into the business. Reinvestment is a fantastic option and usually where I recommend the bulk of business profits be allocated. Forward-thinking business owners know that more capital enables them to pursue the next initiative, test a new strategy, increase marketing efforts, or hire new staff. But, arguably, many business owners reinvest based on hope rather than a calculated risk/return decision. Before reinvesting, be sure to analyze the probable return on investment, the payback period based on cash flow needs, and the opportunity cost of the other available options.

For example…

If you hire another salesperson, what’s the expected return on that investment? What are the cost savings from implementing a new technology platform or strategy? If we spend 10% of our profit on a new client service plan, what is the turnaround time for recouping that investment based on new referrals?

Overall, reinvesting in your business, especially in the years prior to exit planning, is one of the best uses of capital, as long as you’re asking the right questions and doing your homework.

Profits Option #4 – Investing elsewhere

I often tell business owner clients to consistently put a little away on the side. It’s an easy concept but many business owners don’t do it.

Why is investing outside your business a good idea? Here are a couple of examples…

We have a client that owns a retail store. His strategy was to compare the returns our firm could generate to the internal returns of their own business. He wanted an aggressive portfolio. He’d say, “Why would I want to invest outside my business if I can’t make the same rate of return?” Seems logical. However, in March of 2009, we had a conversation that went something like this…

“Jason, I thought I needed to be aggressive with my portfolio to generate returns equal or better than my business. But with this recession, business is down more than 50% year over year, and my portfolio is also deteriorating. I get it now! I want you to manage a conservative and diversified portfolio that will protect me from market volatility.”

Luckily, we stayed the course through 2010 and his business and portfolio returned to previous values. He shifted his risk/return expectations and we shifted to a more conservative and stable portfolio. This more conservative portfolio is not only a safe haven for his balance sheet, it’s also a pool of money that he can access during tough times to support business operations, or better yet, spend on marketing when everyone else is cutting their marketing budget. Advertising rates are very low during recessions!

My next story starts with an absolute truth. It may be voluntarily or involuntarily, but at some point, you’re going to stop working. And when you do, you’re going to need to replace your income.

I worked with a client for 10 years building an investment portfolio outside his business. From day one, he wanted to focus on creating a residual income stream, even though he didn’t need it at the time. He wanted to let his money work for him and he only wanted to invest in what someday would be his only source of income outside of social security. I explained that with a longer time horizon, he could benefit from growth investing; and I explained that at some point, he would sell his business and need to invest the proceeds into a portfolio that could produce retirement income. Thankfully he listened.

So, we spent some time projecting what his finances would look like once he sold his business. We ran some hypothetical income models and tracked the portfolio values. Now he’s been through two recessions and numerous shorter business cycles building an income portfolio. Today, he’s diligent in saving outside his business and currently has more of his investable net worth outside of his business equity. He planned to have sold his business by now, but he hasn’t lost his drive and can afford to wait for just the right buyer. In the meantime, he’s preparing to go through a rising rate environment with his retirement portfolio before he’s retired—which is a case study in itself. Most business owners spend their careers reinvesting in their business, paying off debt and enjoying an increasingly expensive lifestyle. He has already built his retirement portfolio and could walk away at any time. Now he has the freedom to enjoy going to work because he doesn’t have to.

I mentioned at the beginning that I would give a priority list of what to do with your business profits. Here it is:

1. Calculate your reinvestment returns

2. Reinvest half into your business if your expected return is greater than 15%. If you can’t find ways to generate 15%, don’t reinvest anything and start exit planning.

3. Get your debt levels below your industry averages and competitors by paying off debt with the remaining 50%. Once you’ve reached those ratios, don’t pay off debt faster than scheduled unless rates aren’t competitive.

4. Spend 25% on discretionary lifestyle expenses. Take a trip, buy your spouse a gift, buy yourself a gift, finish the landscaping, buy the expensive camera, join the country club, etc.

5. Invest 25% outside your business. Someday, this is the only source of income you will have and you need to understand it, appreciate it, and make good decisions with it.

Jason Wheeler is currently the CEO and a Wealth Consultant at Pathfinder Wealth Consulting. Pathfinder specializes in comprehensive financial, estate and tax planning services, investment management, and risk management (insurance) for business owners and successful executives. Jason Wheeler offers securities and advisory services through Commonwealth Financial Network®. Member FINRA, SIPC, a Registered Investment Adviser. To learn more about Pathfinder Wealth Consulting, visit www.pathfinderwc.com. Jason can be reached at [email protected] or 910-793-0616.

Coastal Land Trust Strikes Deal To Preserve More Than 3,200 Acres Of Sledge Forest

Cierra Noffke

-

Jun 25, 2026

|

|

Refinery Project Eyeing Brunswick County Could Bring $500M Investment, 300 Jobs

Emma Dill

-

Jun 26, 2026

|

|

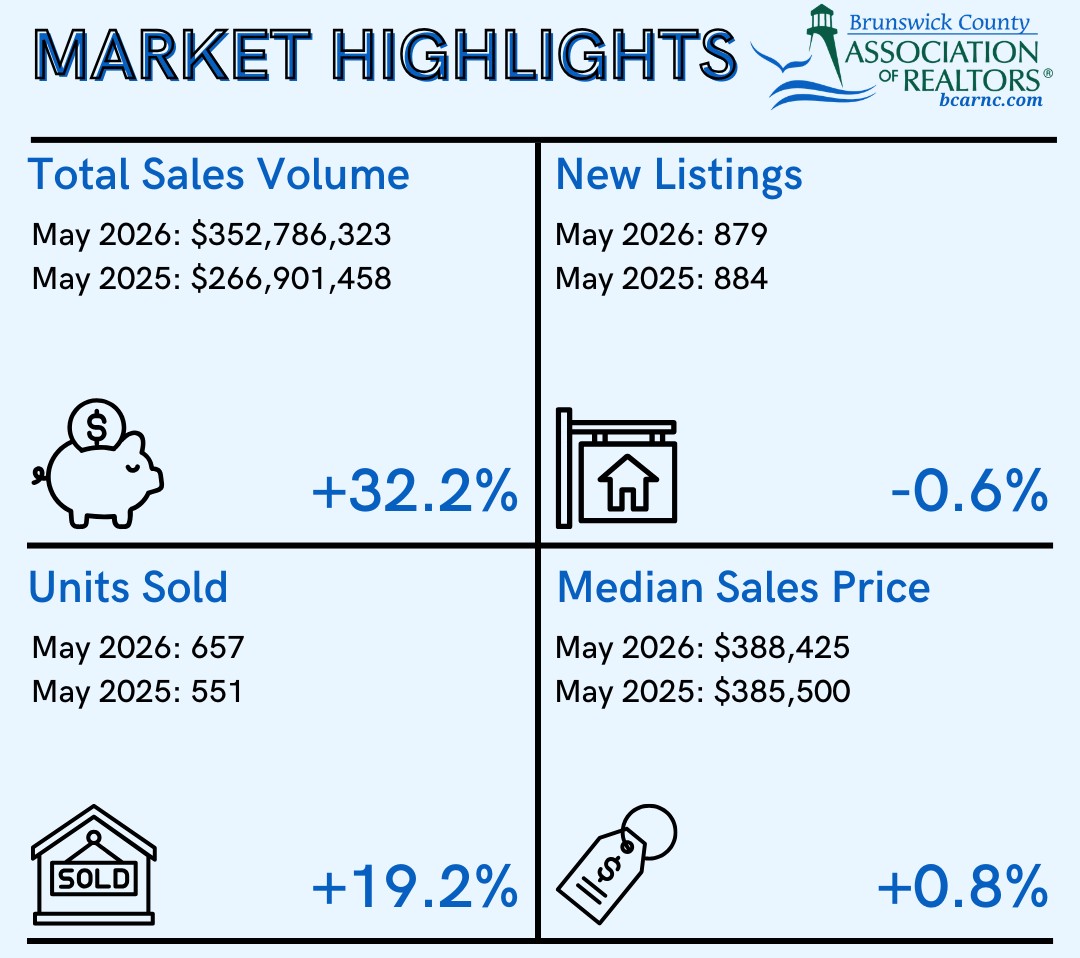

Brunswick Realtors: Home Sales Hit New High In May

Staff Reports

-

Jun 26, 2026

|

|

As Local Firms Exit State Incentive Deals, 2 Remain Active

Emma Dill

-

Jun 25, 2026

|

|

This spring and summer have been a rough time for the city of Southport’s Parks & Recreation Department....

In the past six months alone, a broker with Intracoastal Realty Corp. said he’s sold four lots in the Brooklyn Arts District corridor....

Creative reuse centers, which function like thrift stores, collect donated materials and resell them to the public at discounted prices to b...

The 2026 WilmingtonBiz: Book on Business is an annual publication showcasing the Wilmington region as a center of business.