The Tax Cuts and Jobs Act of 2017 was the most significant piece of tax legislation in the United States in years, which came with many changes, itemized deductions being no exception.

Throughout this article, we will cover the major changes in taxes, charitable and miscellaneous deductions, all of which should be taken into account as we take one final look at tax planning for 2018.

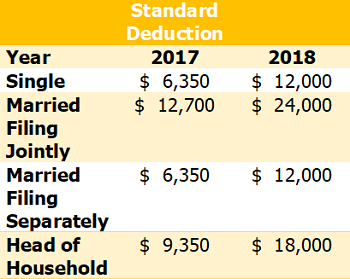

One of the most significant changes is the increase in standard deduction. With an increase in standard deduction, itemizing may be a challenge for some taxpayers in 2018. In addition to the increased standard deduction, the taxes deduction has been capped at $10,000, which includes property taxes and state income taxes paid (sales tax can be substituted for state income tax).

Charitable deductions are still deductible under the new tax legislation. However, the percentage of adjusted gross income (AGI) limit on the deductions for cash gifts to public charities has increased from 50 percent to 60 percent in 2018. With the charitable deduction AGI limit being increased, donor-advised funds are an excellent way to plan your charitable contributions, while also optimizing your charitable donation deduction in the year the donor-advised fund is funded. One way to use a donor-advised fund to your benefit would be to fund it in 2018, which would allow you to take the full amount funded in 2018 as a charitable deduction, then take the standard deduction in 2019 and 2020, while still donating to charities from the donor-advised fund.

Example: A taxpayer who is married filing joint ($24,000 standard deduction), has no medical deductions, his or her taxes deduction is capped at $10,000, and he or she normally give $10,000 to charities. This would not put them over the standard deduction limit.

However, if they funded a donor-advised fund in 2018 with the next three years of charitable donations ($10,000/year x 3 years = $30,000 total), this would put them over the threshold for itemized deductions. They will itemize with $10,000 tax deduction + $30,000 charitable deduction = $40,000 total itemized deduction versus the standard deduction of $24,000.

The taxpayer would then take the standard deduction in 2019 and 2020. This would increase their deduction by $16,000 between 2018-2020 versus just taking the standard deduction all three years.

Lastly, miscellaneous deductions, which used to be deductible if exceeding two percent of a taxpayer’s AGI, are no longer deductible. Miscellaneous deductions included unreimbursed employee expenses, tax preparation fees and other expenses (investment expense, safe deposit box, etc.).

All these considerations put a new emphasis on understanding your individual tax position. For these reasons, planning with your tax professional is more important than ever. I urge you to obtain professional advice on your personal tax situation before acting on any of the information discussed above.

Ryan Skuce joined Earney & Company, L.L.P. in 2003, and became a partner in November 2013. He works extensively with physicians, medical practices, and large medical groups. Ryan has experience in accounting and tax services including financial reporting and analysis, technical support, cash flow planning, physician compensation strategies, and medical practice strategic planning. He also has experience in the areas of accounting and tax for a variety of for profit and nonprofit clients. Ryan is currently a member of the American Institute of Certified Public Accountants (AICPA) and the North Carolina Association of Certified Public Accountants (NCACPA). Ryan works with his clients on evaluating operational and technical issues. He provides back-office accounting support, and recommends and assists in the implementation of ideas to cut overhead costs and streamline operations. With an in-depth knowledge of existing and proposed tax laws, Ryan often advises companies on tax deferment or savings through proactive structuring of transactions. He also assists his clients with Internal Revenue Service audits. He received his Masters of Science in Accountancy from UNC-Wilmington and resides in Wilmington, where he enjoys playing hockey with a local team.