Jeff Stokley recently went through the health insurance renewal process for two of the Wilmington-based companies he leads – Advanced Air Solutions and Noelle LLC.

“Every year, it’s always a huge increase. We had to really increase deductibles because of the increase in premiums, and of course the cost of the business just keeps going up and up,” he said.

The deductible for employees in their plan now is about $5,000.

“We partially self-fund half of that with them, but we’re taking a risk on how many claims the employees will have each year,” Stokley said.

A heating and air and mold remediation company, Advanced Air Solutions has 25 employees, and Noelle LLC, a women’s clothing and accessory manufacturer and wholesaler, has 75. Stokley’s companies are not alone in the struggle.

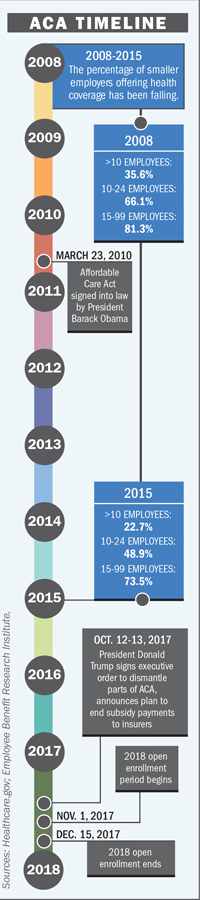

Since a couple years before the Affordable Care Act was enacted in 2010, the percentage of small businesses that offer any health coverage at all has been falling, and some small business owners say they’ve been hit particularly hard by what they see as ACA’s disadvantages in the form of higher premiums and deductibles.

When one of Stokley’s companies loses a worker, they’re often replaced with a temporary employee.

“Therefore our workforce has actually been reduced in a lot of our departments in both companies,” he said.

He said he hopes lawmakers can eventually come together on the issue “and know that this is severely affecting small businesses … It hurts the workforce because they’re not getting full-time employment and benefits.”

At one time, Rex Creech, owner of Rex & Sons RV, paid half of the insurance for the company’s employees “and that worked out real well … and then they put in Obamacare [another name for ACA], and they could buy it a little cheaper than we could as a group so we’ve done away with our group. And now it’s about four times as high as it’s ever been and they can’t afford it,” Creech said.

“We have the same problem everybody else is having. It’s a shame; it really is,” said Creech, whose business has 14 employees.

Hank Estep, principal agent at GriffinEstep, an independent insurance brokerage firm based in Wilmington, and Larry Grudzien, an ACA attorney who works with companies like Estep’s across the country, described recent efforts to change ACA and even proposals before that seeking to address the issue of health coverage in the U.S., as “rearranging the deck chairs on the Titanic.”

The sinking ship they’re comparing to the Titanic is the enormous cost of health care, a complex issue not likely to be resolved soon.

Creech said a stress test for a heart checkup he took several years ago cost him less than $70 in a copay at the time. More recently, he was quoted an out-of-pocket cost of $1,500.

“I won’t be having another stress test I guess,” Creech said. “I’ll kick the bucket before I do that again.”

Estep said consumers cut back when the costs get too high, asking themselves questions such as, “Do I really need this prescription or this MRI?”

Officials with some of Wilmington’s largest health care providers say one of their goals is to make care more affordable.

In the meantime, there is some good news: While insurance rates increase every year, that rise this year was in the single percentage point range, Estep said, rather than the double digits some employers had been experiencing.

On Oct. 12, President Donald Trump, who has been vocal about his frustrations with the inability of Congress to approve an overhaul to ACA, signed an executive order that impacts the law’s provisions. According to news reports, the order instructs Cabinet officials to rewrite federal rules for association health plans. For those plans, small businesses band together through an association to negotiate health insurance coverage.

The order’s aim is to relax some of the restrictions the ACA places on associations. The problem with associations, Estep said, is that many of them end up falling apart.

Giving an example, Estep said, “Let’s say there’s an association with 100 small employers and now let’s say the average size is 20 [employees] … let’s say one of the 100 has no claims risk at all; they’re squeaky clean. A competing insurance company will go to that 20-employee group [to offer a lower price] so that one single group will leave, and then over time another will leave.”

Meanwhile, the companies with more health problems stay in the association because no competing insurance company wants them, and their rates can increase.

“An association almost always dissolves over time,” Estep said.

Among the financial issues faced by ACA was that from the outset, not enough young people who don’t already have health problems signed up, Grudzien said.

“The money’s got to come from someplace. It’s wonderful that people are taken care of, but it comes at a cost,” he said.

In 2014, ACA subsidies started coming in from the government, and that year and the next a lot of small firms were dissolving their group plans and directing people to the ACA exchanges. But since 2015, because insurance companies ended up losing a lot of money on high claims, those firms increased their rates, Estep said.

“The subsidies are still there, but the rate differential between what the subsidy was paying and the real rate has expanded,” he said.

In North Carolina, the only insurer left on the ACA exchange is Blue Cross Blue Shield of North Carolina, with more than 500,000 state residents on the company’s ACA plan, according to the insurer. The firm’s latest rate hike request is 14.1 percent, which had not been approved yet by the N.C. Department of Insurance as of press time.

For small businesses that still want a group plan, they have six options in North Carolina, Estep said: Blue Cross, UnitedHealthCare, Cigna, Aetna, First Carolina Care and self-funding with stop-loss insurance.

“It behooves them to bid it out,” Estep said, “and get all the carriers to provide quotes.”

For more on how local health care provider are making plans while faced with the ACA's uncertain future, click here.